Government & Compliance Audits

Government & Compliance Audits SOC 1

SOC 1 SOC 2

SOC 2 SOC 3

SOC 3 Subrecipient Monitoring Services

Subrecipient Monitoring Services Attestation Engagements

Attestation Engagements Employee Benefits Plans (ERISA)

Employee Benefits Plans (ERISA) HIPAA

HIPAA SOC for Supply Chain

SOC for Supply Chain  SOC for Cloud Security

SOC for Cloud Security Grant Compliance Consulting

Grant Compliance Consulting NIST

NIST SOC

SOC Business Strategy & Excellence

Business Strategy & Excellence Business Intelligence & Data Analytics

Business Intelligence & Data Analytics Application Control Testing

Application Control Testing Bookkeeping

Bookkeeping Daily Operations

Daily Operations Outsourced CFO & Advisory

Outsourced CFO & Advisory Tax Planning

Tax Planning Tax Reporting

Tax Reporting IRS & FTB Representation

IRS & FTB Representation Tax Strategy & Compliance

Tax Strategy & Compliance Corporate Tax Provisions ASC 740

Corporate Tax Provisions ASC 740 Nonprofit & Tax-Exempt

Nonprofit & Tax-Exempt

Key Takeways

- Operational and internal control reviews check how well a business’s systems, policies, and people prevent errors, detect fraud, and support compliance.

- Common financial processes that create compliance risks for California businesses are payroll, billing, procurement, and reconciliation.

- At The Pun Group, we help organizations find operational risks, tighten controls, and prepare for audits through internal control reviews and our subrecipient monitoring services.

What Are Operational and Internal Control Reviews?

An operational and internal control review is a structured evaluation of how well a business manages risk, maintains efficiency, and protects its resources through the systems and procedures that guide day-to-day operations.

These reviews help business leaders in cities like Los Angeles and San Diego optimize operational efficiency and resource allocation.

They evaluate the following:

- How operational and internal controls work together to support business objectives, ensure compliance, and prevent disruptions.

- Whether the company’s internal policies and operational procedures are documented, enforced, monitored, and effective.

- Compliance with internal policies, industry standards, and applicable laws.

- Improvements needed to safeguard assets, enhance accuracy, and support decision-making.

This review involves examining the business’s control environment (like the policies governing financial reporting, access to assets, or vendor payments). It also involves reviewing the operational mechanisms that put those policies into action, like system access rules, change management protocols, and incident response plans.

Key Financial Processes Subject To Review in California Businesses

Financial processes are the backbone of business operations. But they’re also where most compliance violations, fraud, and operational inefficiencies occur. California’s strict regulatory environment makes these processes critical to monitor, as violations can result in significant penalties, legal exposure, and operational disruptions.

Here are the financial processes subject to internal and operational control reviews for California businesses:

1. Procure-To-Pay (P2P)

Business owners, department heads, and team members must follow best practices for vendor management and third-party relationships.

Procure-to-pay (P2P) covers the full purchasing cycle, which starts with vendor selection and ends with payment. It covers procurement, accounts payable, and compliance, and each step requires control decisions that affect cash flow and fraud risk.

This process is a frequent focus in reviews because it involves many actors and large sums. Gaps in approval chains, vendor vetting, or payment rules often lead to misstatements or regulatory exposure.

California law puts many parts of this chain under review. For instance, under AB 5 (CA Labor Code § 2750.3), companies have to make sure vendors classified as independent contractors pass the ABC test.

Purchase orders also have to follow dual-approval rules for large amounts, which can reduce fraud risk under CA Penal Code § 504.

2. Order-To-Cash (O2C)

Order-to-cash (O2C) covers the process of receiving customer orders, issuing invoices, collecting payments, and recording revenue. It includes billing systems, accounts receivable, and cash management.

O2C is linked directly to revenue reporting and liquidity, so errors or control gaps here can result in misstated income, uncollected balances, and compliance failures. Customer satisfaction and customer experience also depend on accurate billing and quick response times.

For California businesses, the Automatic Renewal Law (ARL) requires clear, upfront disclosures for recurring charges, which are common in SaaS and subscription models. Noncompliance can lead to chargebacks or legal complaints.

3. Payroll and Timekeeping

Payroll and timekeeping processes handle wage calculations, tax withholdings, and benefit deductions. They rely on accurate time records, employee classification, and up-to-date legal compliance.

This area is heavily regulated in California. Auditors review it closely because errors can lead to costly penalties, wage claims, or employee disputes.

Unlike federal law, California’s Labor Code § 510 requires daily overtime pay after eight hours of work. Missing these can trigger underpayment claims.

Businesses also need to classify workers correctly. Misclassifying full-time employees as independent contractors, which is payroll fraud, may result in back wages, unpaid taxes, and fines.

4. General Ledger and Financial Reporting

This process records all financial activity into the general ledger and produces the financial statements. It includes journal entries, account reconciliations, and month-end close procedures.

In California, this process is always under review because small errors or manual overrides can distort reporting or hide fraud. This is why, under California law, companies have to:

- Make sure journal entries follow documented approval workflows. For public companies, the Sarbanes-Oxley (SOX) Act’s Section 404 requires documentation of controls around entries

- Ensure monthly reconciliations are accurate because delays or skipped reviews can hide unauthorized transfers or missing cash

5. Budgeting and Forecasting

Budgeting and forecasting guide how organizations plan for expenses, allocate resources, and evaluate performance. This process includes annual budgets, rolling forecasts, and variance analysis.

California imposes strict budgeting and forecasting requirements for many sectors. For instance, Government Code § 13400 requires balanced budgets and multi-year forecasts for public agencies and contractors receiving state funds.

6. Capital Expenditures (CapEx)

Capital expenditures involve the purchase or upgrade of long-term assets like equipment, vehicles, or software, all of which often require large sums and long-term planning. These assets are recorded on the balance sheet and depreciated over time.

CapEx reviews focus on approval workflows, supporting documentation, and proper classification. Mistakes here can affect financial reporting, tax filings, and compliance with state rules.

7. Tax Compliance and Reporting

Tax compliance reviews focus on how businesses calculate, report, and pay their required taxes. This includes sales tax, franchise tax, and information returns like 1099s.

In California, sales and use tax enforcement is active and complex. The California Department of Tax and Fee Administration (CDTFA) requires businesses to collect tax on digital goods under RTC § 60050.

Franchise tax rules also apply to all corporate entities. The Franchise Tax Board (FTB) charges 8.84% for C-corporations and 1.5% for S-corporations. Missed or underpaid taxes can often lead to Franchise Tax Board (FTB) audits.

Aside from that, businesses that issue 1099s have to make sure contractors meet California’s ABC test under AB 5. Any misclassifications can lead to penalties, back taxes, and disallowed deductions.

8. Cash and Treasury Management

Cash and treasury management includes monitoring bank activity, managing liquidity, and handling payments like wire transfers. Strong controls in this area protect against fraud, ensure solvency, and support daily operations.

California businesses face a lot of risk if bank reconciliations are delayed or poorly reviewed. For instance, under CA Penal Code § 502, tampering with financial data, including false reconciliations, can carry criminal liability.

9. Expense Reimbursements

This process covers how employees get reimbursed for work-related expenses and how corporate cards are issued and managed. Weak controls here often lead to unapproved spending, missing receipts, and policy violations.

In California, Labor Code § 2802 requires employers to fully reimburse necessary business expenses, everything from travel costs to phone bills. Reimbursement rates, like mileage, have to meet current California standards, with delays or denials triggering wage claims.

The state also disallows unsubstantiated expenses. This means that if employees submit vague or incomplete reports, your business can run into compliance issues and potential penalties during financial audits.

Common Compliance Risks in California Found During Reviews

California has some of the strictest financial laws in the country, which makes compliance very difficult for companies. Here are common compliance risks for businesses in California:

1. Payroll Violations

California labor law is stricter than federal standards. Employers have to follow daily overtime rules, meal/rest break requirements, and final paycheck deadlines. Under AB 5, many gig workers now qualify as employees, which means payroll tax and benefits obligations.

Small oversights, like missing break logs or late final pay, can lead to class-action lawsuits or Labor Commissioner audits.

2. Sales Tax Errors (CDTFA)

California’s sales tax system includes a state base rate and layered district taxes that vary depending on the city or county. Businesses have to collect and remit the correct amount, not just statewide, but locally.

Since the California Department of Tax and Fee Administration (CDTFA) aggressively audits misclassified revenue, a missing local tax rate or an outdated POS system can trigger penalties, interest, and multi-year audits.

3. P2P Fraud (Vendor/AP)

Procure-to-pay fraud often starts with weak controls, like missing vendor approval steps, a lack of segregation, or a single-person payment authority.

Small and mid-sized California businesses are usually the most affected because they may skip dual-approval protocols for speed or convenience. They may be at risk of fraud tactics like fake vendors, inflated invoices, or diverted payments. All of these can trigger penalties.

4. Auto-Renewal Law Violations

California’s Automatic Renewal Law (ARL) requires clear, upfront disclosure of all material terms before obtaining consumer consent, including the automatic renewal provision, cancellation policy, and recurring charges.

Many businesses violate these requirements by using deceptive “dark patterns.” Examples include pre-checked boxes, hidden terms in fine print, or making cancellation processes unnecessarily difficult, such as requiring phone calls when the subscription was purchased online.

The California Attorney General and local district attorneys can impose fines of up to $2,500 per violation. This means a subscription service with thousands of California customers could face devastating financial penalties for non-compliance.

5. Misclassified Contractors (AB 5)

California’s Assembly Bill 5 (AB5) requires workers to pass the ABC test to determine their classification. It presumes all workers are employees unless the hiring entity can prove the worker:

- Is free from company control

- Performs work outside the hiring entity’s usual business

- Is customarily engaged in an independent trade

Businesses that misclassify employees as contractors face liability for back wages, overtime, payroll taxes, and penalties between $5,000 and $15,000 for each violation under California Labor Code Section 226.8.

6. Unclaimed Property (Escheatment)

California’s Unclaimed Property Law requires businesses to report and remit uncashed checks, unused refunds, and dormant credits after three years of inactivity. This includes vendor payments, customer overpayments, and payroll checks.

Many companies overlook these obligations due to poor recordkeeping or system gaps. This noncompliance can trigger audits, penalties, and forced remittances.

7. Bank Reconciliation Gaps

In California, embezzlement through falsified bank records can lead to charges under Penal Code § 502.

Many small businesses lack oversight here and usually don’t have any second reviewer, monthly cutoff, or audit trail. This may create unusual adjustments, missing backups, or delays in reconciling cash activity, which can threaten their liquidity and legal standing.

8. Expense Reimbursement Failures

California law requires employers to repay all necessary business expenses under Labor Code § 2802. This includes travel, mileage, and supplies. Reimbursements without receipts or policy enforcement often go unreviewed, which may open the door to fraud or wage claims.

Since many companies don’t set mileage limits or verify supporting documentation, they end up with missing logs, handwritten notes, or vague justifications. All of these can lead to compliance issues.

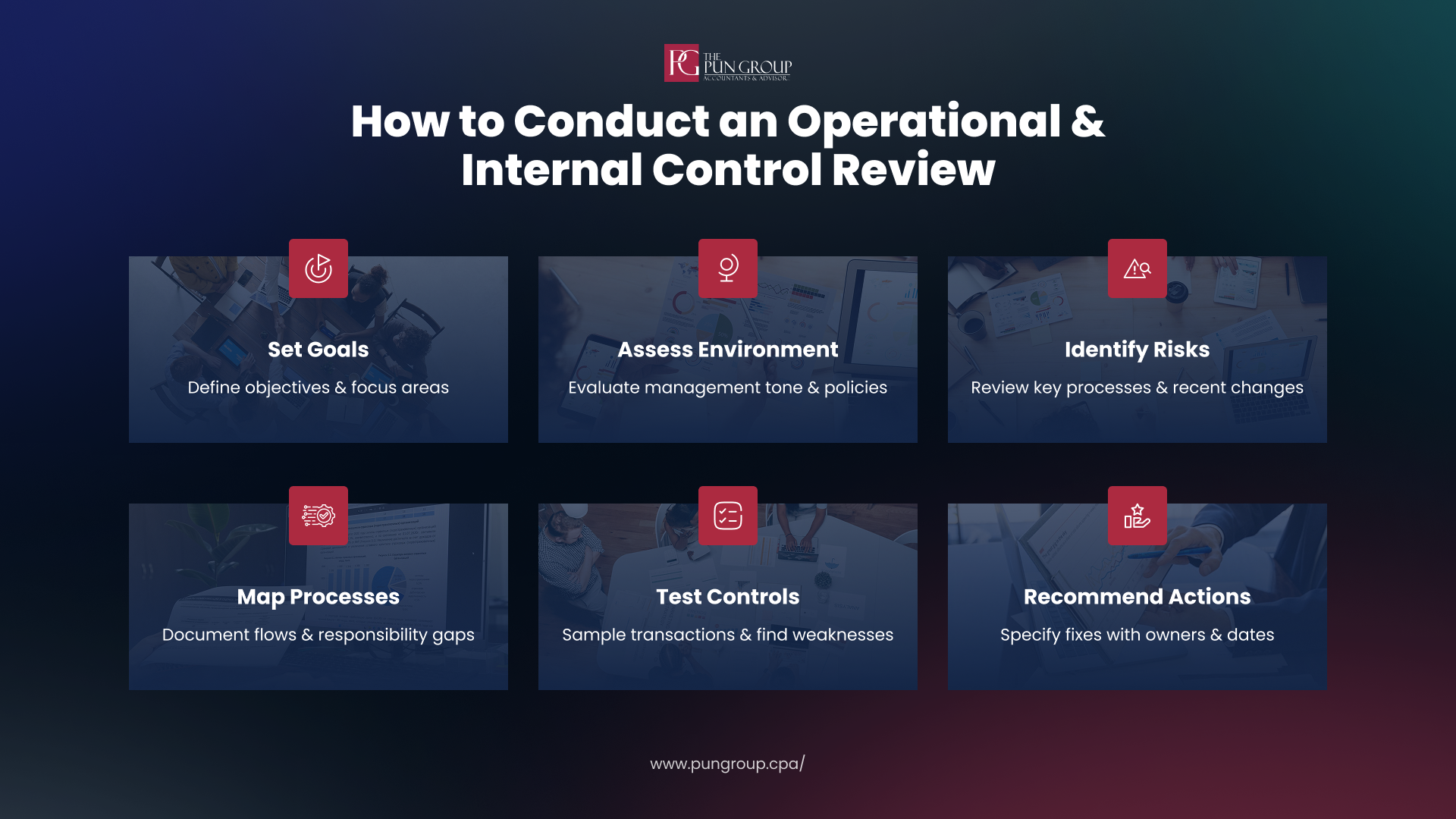

Steps To Conduct an Effective Operational and Internal Control Review

An effective operational and internal control review checks how well an organization prevents risk, manages resources, and meets compliance obligations, without burdening daily operations. Here’s how to perform it:

1. Set the Review Goals

Every review needs a purpose. As the first step, think about what you want to achieve. Do you want to reduce fraud risk, find misclassified expenses, or evaluate regulatory compliance?

Your goals should connect directly to known risk areas or recent issues. For example, if leadership turnover recently occurred, the review could focus on approvals and segregation of duties.

2. Understand the Control Environment

You need to understand the control environment to learn how effective it is. If leadership doesn’t take operational and internal controls seriously, no checklist or policy will fix this.

Start by looking at how management sets the tone. Are executives trained on compliance requirements like Assembly Bill 5, CCPA, or procurement ethics under Gov. Code § 1090? Do supervisors model responsible behavior or bypass controls themselves?

You should also check if the organization has an audit committee or internal control lead, ethics policies, conflict of interest disclosures, and employee handbooks that outline expectations.

3. Identify and Assess Risks

Once you understand the operational and internal control environment, you need to understand the operational and financial risks connected to key activities like payroll, vendor payments, budgeting, revenue, and IT systems.

After that, look for recent changes, like new hires, funding shifts, or technology rollouts. These often create risks that need immediate attention.

4. Map Key Processes and Transactions

Before testing controls, you need to understand how transactions flow. Process mapping can help you understand who touches a transaction, what systems are involved, and where risks can sneak in.

You need to start with one area and then work through it. For example, for accounts payable, you need to know who selects vendors, issues purchase orders, verifies invoices, cuts checks, and reconciles bank statements. If one person does too many of these steps, that’s a red flag.

You can use flowcharts or swimlane diagrams to track each handoff, especially for payroll, vendor onboarding, expense reimbursements, bank reconciliations, and sales tax handling. Mapping these flows can help you see where controls exist and where they don’t.

5. Evaluate Existing Controls

Now that you know how processes flow, check what controls exist and test how well they work. You need to start with policies and check if they’re documented, current, and if employees know they exist.

Once you understand the current policies, test how those controls function. You should focus on areas with a history of errors, fraud, or audit findings.

To go deeper, interview staff, pull samples, and look for control overrides, missing documentation, or signs that “workarounds” are the norm. You can also use reconciliations, variance analysis, and exception reports to test performance and look for historical patterns.

6. Recommend Corrective Actions

Once you’ve gone over the controls, state what was tested, what failed, and what needs to happen next. You could organize findings by risk area (like payroll, procurement, billing, reporting) and explain:

- The control gap (like missing approval logs)

- The risk it creates (such as fraud or noncompliance)

- The related law or policy (e.g., Labor Code § 203, Gov. Code § 13400)

- A recommendation (like “require written supervisor sign-off for all timesheets”)

You should recommend fixes that reduce risk without slowing down operations, assign responsibility for each fix, and set follow-up dates. A review has no value unless its findings lead to change.

Note that these steps apply to general business operations. Grant recipients and their subrecipients face additional layers of federal compliance requirements that demand specialized expertise. Federal regulations require prime recipients to monitor their subrecipients to ensure proper use of grant funds and compliance with complex federal guidelines.

At The Pun Group, we conduct comprehensive assessments that include federal compliance verification, risk analysis, on-site monitoring, and corrective action planning. Our team understands grant management challenges and helps organizations maintain funding security while building sustainable compliance frameworks.

Let The Pun Group Help You Perform Operational and Internal Control Reviews

Operational and internal control reviews prevent wage lawsuits, sales tax penalties, and vendor fraud before they happen. For grant recipients, subrecipient monitoring ensures federal compliance and protects your funding from costly violations.

But building reviews and monitoring systems that actually work is another matter. It takes time, technical skill, and deep knowledge of California’s regulations and federal grant requirements. That’s where The Pun Group comes in.

At The Pun Group, we help California businesses and grant recipients find control gaps, improve compliance, and build audit-ready systems without slowing down operations. Here’s how we do it:

- We map and test high-risk processes, going straight to your payroll cycles, vendor payments, reconciliations, and reporting systems to spot weak points.

- We conduct comprehensive federal compliance assessments using proven methodologies.

- We develop corrective action plans and provide ongoing support to maintain compliance.

Want to learn more about how we can help you with business success? Contact The Pun Group to schedule a risk-focused review or monitoring assessment that works for your organization!