Government & Compliance Audits

Government & Compliance Audits SOC 1

SOC 1 SOC 2

SOC 2 SOC 3

SOC 3 Subrecipient Monitoring Services

Subrecipient Monitoring Services Attestation Engagements

Attestation Engagements Employee Benefits Plans (ERISA)

Employee Benefits Plans (ERISA) HIPAA

HIPAA SOC for Supply Chain

SOC for Supply Chain  SOC for Cloud Security

SOC for Cloud Security Grant Compliance Consulting

Grant Compliance Consulting NIST

NIST SOC

SOC Business Strategy & Excellence

Business Strategy & Excellence Business Intelligence & Data Analytics

Business Intelligence & Data Analytics Application Control Testing

Application Control Testing Bookkeeping

Bookkeeping Daily Operations

Daily Operations Outsourced CFO & Advisory

Outsourced CFO & Advisory Tax Planning

Tax Planning Tax Reporting

Tax Reporting IRS & FTB Representation

IRS & FTB Representation Tax Strategy & Compliance

Tax Strategy & Compliance Corporate Tax Provisions ASC 740

Corporate Tax Provisions ASC 740 Nonprofit & Tax-Exempt

Nonprofit & Tax-Exempt

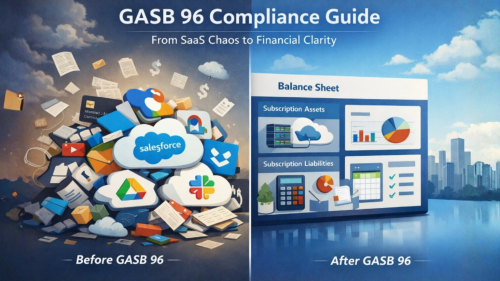

Let’s be honest — when most people hear “accounting standard update,” their eyes glaze over. But if you work in government finance or manage IT contracts for a public entity, GASB 96 is one update you really can’t afford to sleep on.

Here’s the short version: governments use a lot of subscription-based software these days — think Microsoft 365, Salesforce, Dropbox, cloud-based HR systems, and more. For years, most of those payments were simply expensed and forgotten. GASB 96 changed that. Now, those arrangements need to show up on your financial statements in a very specific way.

In this guide, we’ll walk you through what GASB 96 actually means, who it applies to, what you need to do, and — importantly — the common mistakes that trip governments up during audits.

First, What Exactly Is GASB 96?

GASB Statement No. 96 was issued by the Governmental Accounting Standards Board to address a gap that had been growing for years: governments were increasingly entering into subscription-based IT arrangements, but there were no clear rules for how to account for them.

The standard became effective for fiscal years beginning after June 15, 2022. That means most government entities have already crossed into GASB 96 territory — but not all of them are fully compliant.

At its core, GASB 96 defines a new category called a Subscription-Based Information Technology Arrangement, or SBITA. A SBITA is any contract that gives a government the right to use another party’s IT software — alone or in combination with tangible capital assets — for a defined period of time, in exchange for payment.

Sound familiar? It should. It’s structured similarly to how GASB 87 (the lease standard) works — which makes sense, because the Governmental Accounting Standards Board intentionally modeled it that way for consistency.

Who Does GASB 96 Apply To?

If your organization follows Generally Accepted Accounting Principles (GAAP) and is a public sector entity, GASB 96 applies to you. That includes:

- State and local governments

- School districts

- Public colleges and universities

- Government agencies and authorities

- Public utilities, hospitals, and other government-operated entities

In short: if you’re a government entity paying for software on a subscription basis, this standard is for you.

What Counts as a SBITA?

This is where it gets a little nuanced — and where organizations often make their first mistake. Not every IT contract qualifies as a SBITA. The key test is control.

To be a SBITA, the contract must give the government both:

- The right to obtain the present service capacity from the IT asset, and

- The right to determine the nature and manner of use of that IT asset.

Both conditions must be met. If the vendor controls how and when the software is used, it may not qualify as a SBITA.

Common examples that typically DO qualify:

- Cloud-based ERP and financial management systems

- Hosted productivity suites (email, document collaboration, and video conferencing platforms)

- Cloud-based HR, payroll, and benefits administration systems

- Permitting, licensing, and land management platforms

- Agenda, meeting, and records management systems

- Cloud-based GIS and asset management software

- CRM, case management, and constituent service platforms

- Platform-as-a-Service (PaaS) and Infrastructure-as-a-Service (IaaS) arrangements used to host government applications

What’s excluded:

- Contracts that are already classified as leases under GASB 87

- Perpetual software licenses (those fall under GASB 51)

- Pure IT service contracts with no right to use an underlying asset

- Short-term arrangements with a maximum term of 12 months or less

That last point — the short-term exception — can offer some relief. If a subscription’s maximum possible term (including renewals) is 12 months or less, you can simply expense the payments as you go, without recognizing an asset or liability.

What GASB 96 Actually Requires You to Do

Once you’ve identified your SBITAs, here’s what the standard requires:

1. Recognize a Right-to-Use Subscription Asset

At the start of the subscription term (when the asset is placed into service), you record an intangible asset on your balance sheet — the right to use the software. This asset is amortized over the shorter of the subscription term or the useful life of the underlying IT asset.

2. Recognize a Corresponding Subscription Liability

Alongside the asset, you also recognize a subscription liability measured at the present value of all future subscription payments. That means you’ll need to use an appropriate discount rate — specifically, the interest rate charged by the SBITA vendor (which may be implicit in the contract). If that rate isn’t readily determinable, the government’s incremental borrowing rate is used instead.

3. Account for Implementation Costs by Stage

GASB 96 breaks implementation activities into three stages, and the accounting treatment differs for each:

- Preliminary project stage — costs are expensed as incurred (think: evaluating vendors, deciding whether to proceed)

- Initial implementation stage — costs may be capitalized (think: configuring the system, testing, training)

- Operation and additional implementation stage — costs are generally expensed, unless they add new functionality

Getting this right matters. Miscategorizing costs across stages is one of the most common audit findings.

4. Provide Note Disclosures

Your financial statement footnotes need to include meaningful information about SBITAs, including:

- A general description of the arrangements

- The total subscription liability balance

- Principal and interest requirements for the next five years and in five-year increments thereafter

- Variable or other payments not included in the liability

- Information about SBITAs that have been committed but not yet started

The Most Common GASB 96 Mistakes (and How to Avoid Them)

Here’s what auditors are actually seeing in the field:

Missing SBITAs entirely

SaaS is often purchased outside of IT — by department heads, procurement staff, or even individual employees using a credit card. Without a centralized inventory, many arrangements fall through the cracks. You need a complete picture of every subscription in your organization, regardless of how it was purchased or who approved it.

Miscoding subscription payments

A significant number of SaaS purchases are coded as something other than software in accounting systems — office supplies, professional services, miscellaneous expenses. If it’s not coded correctly, it won’t show up in your SBITA inventory. Reviewing transaction data and vendor contracts together is the only reliable way to catch these.

Incorrect discount rate selection

Choosing the wrong rate to calculate the present value of subscription payments can materially misstate your liability. The standard calls first for the interest rate the vendor charges the government (implicit or stated), and only falls back to the incremental borrowing rate if the vendor rate is not readily determinable. This requires judgment and documentation.

Mixing up implementation cost stages

As mentioned above, the three-stage framework for implementation costs requires careful classification. Expensing costs that should be capitalized (or vice versa) leads to audit adjustments and restatements. When in doubt, document your rationale clearly.

Thin or incomplete disclosures

Some entities recognize the asset and liability correctly but then fail to provide adequate note disclosures. Auditors look closely at this. The notes should give readers a clear picture of your SBITA obligations — not just a single line item.

How to Actually Prepare: A Practical Checklist

If you want to walk into your next audit with confidence, here’s where to start:

- Build a complete SBITA inventory — pull contracts from IT, finance, procurement, and department heads. Look for anything subscription-based that involves software access.

- Review contract terms carefully — determine whether each contract gives you control over the underlying IT asset, which is the threshold for SBITA classification.

- Apply the short-term exception where appropriate — if a subscription’s maximum possible term is 12 months or less, you can simplify your accounting treatment.

- Determine your discount rate — document your incremental borrowing rate and apply it consistently across all qualifying SBITAs.

- Categorize implementation costs by stage — map your setup and rollout activities to the three stages and document which costs are being capitalized versus expensed.

- Build your disclosure template — work with your finance team or CPA to ensure footnote disclosures are thorough and meet GASB 96 requirements.

- Establish a recurring review process — SBITAs change. Contracts renew, terms get modified, new subscriptions get added. Set a process to review and update your inventory at least annually.

The Bottom Line

GASB 96 isn’t going away, and neither is the government’s reliance on subscription software. If anything, the number of SBITAs in most government entities is only going to grow as more services move to the cloud.

The good news? This is entirely manageable with the right process and the right team. The key is being proactive — identifying your arrangements, getting your accounting right the first time, and keeping your documentation organized so the audit process runs smoothly.

If your organization is still working through GASB 96 implementation, we’d be glad to talk through common pitfalls and answer questions about SBITA classification, measurement, and disclosure.

The Pun Group serves government entities and compliance-focused organizations across California, Nevada, Arizona, and Hawaii. Reach out to our team to talk through where you stand.